AI-Powered Early Warning Systems: Transforming Credit and Operational Risk Management

Introduction: The Shift from Reactive to Proactive Risk Management

Banking institutions face a critical challenge: detecting risk signals before they escalate into significant losses. Traditional risk management was reactive, relying on periodic reviews that often identify problems only after deterioration begins. The global banking sector recorded over USD 500 billion in cumulative operational risk losses, while cybercrime losses reached USD 20.9 billion in the U.S. in 2025, up 26% year-over-year [1]. These figures underscore a fundamental truth: delayed risk detection costs far exceed prevention investments. AI-powered early warning systems represent a paradigm shift, continuously monitoring market conditions, financial metrics, operational behaviors, and covenant compliance across entire portfolios. By combining rule-based logic with advanced signal processing, modern systems detect stress indicators weeks or months before traditional methods. This proactive approach enables early intervention with targeted mitigation strategies, transforming risk management from damage control into value preservation—now essential for competitive survival.

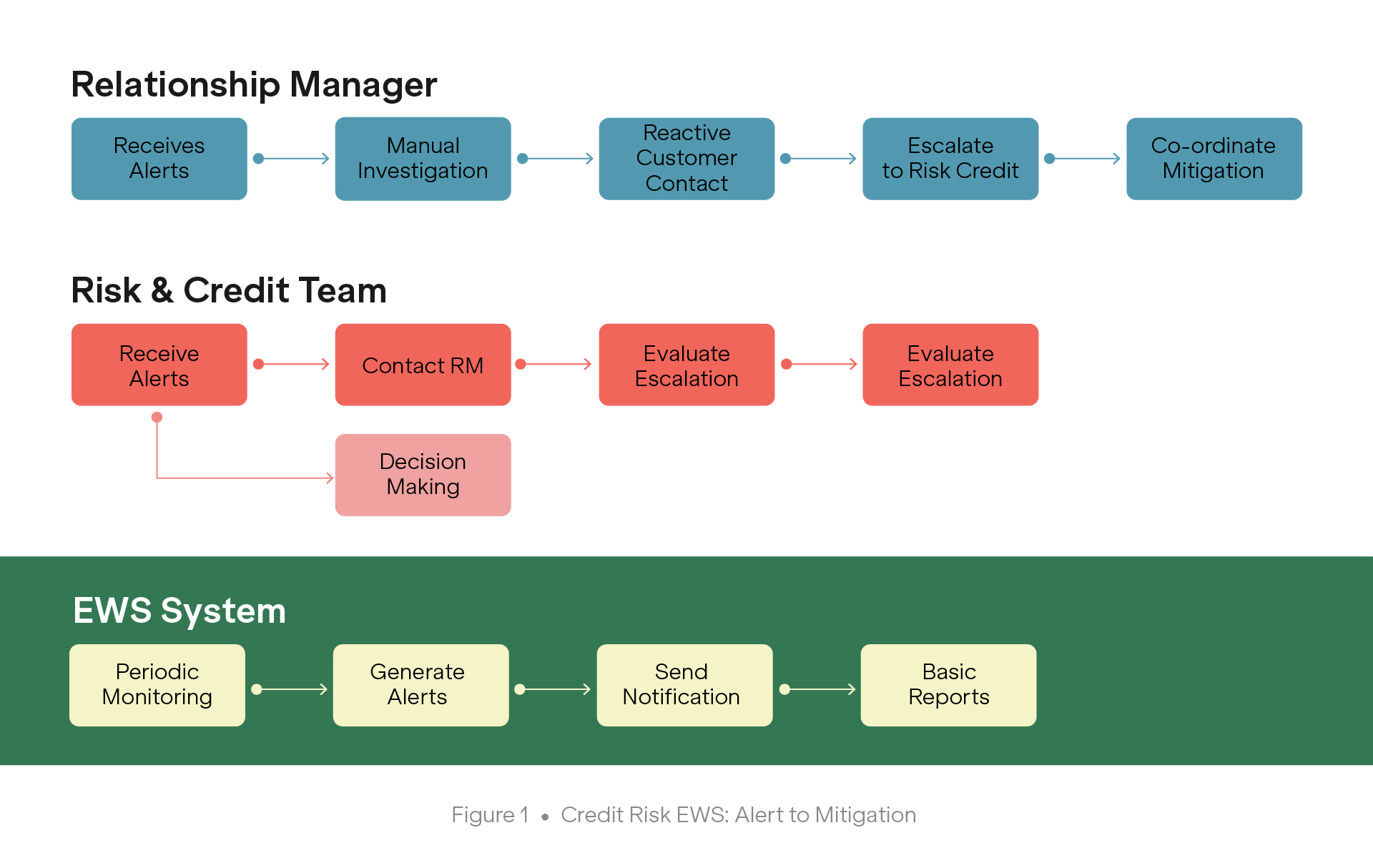

Credit Risk Management: From Manual Reviews to Intelligent Monitoring

Credit risk assessment has traditionally relied on historical repayment patterns and static credit scores. These methods capture only backward-looking data and update infrequently. The banking sector is projected to spend over USD 73 billion on AI technologies by end of 2025, a 17% increase, with credit risk management a top priority [2]. AI-driven platforms analyze multiple signal categories:

payment behaviors, financial stress indicators like declining revenue, covenant compliance, and market intelligence from news and regulatory alerts. By correlating weak signals, AI systems identify deterioration patterns invisible in conventional analysis—for example, a borrower maintaining payments while experiencing stock declines, management turnover, and delayed filings [1]. This approach distinguishes temporary liquidity challenges from structural insolvency. AI-driven modeling improves loan approval accuracy by 34% in mid-size banks while reducing false positives by up to 80% [2].

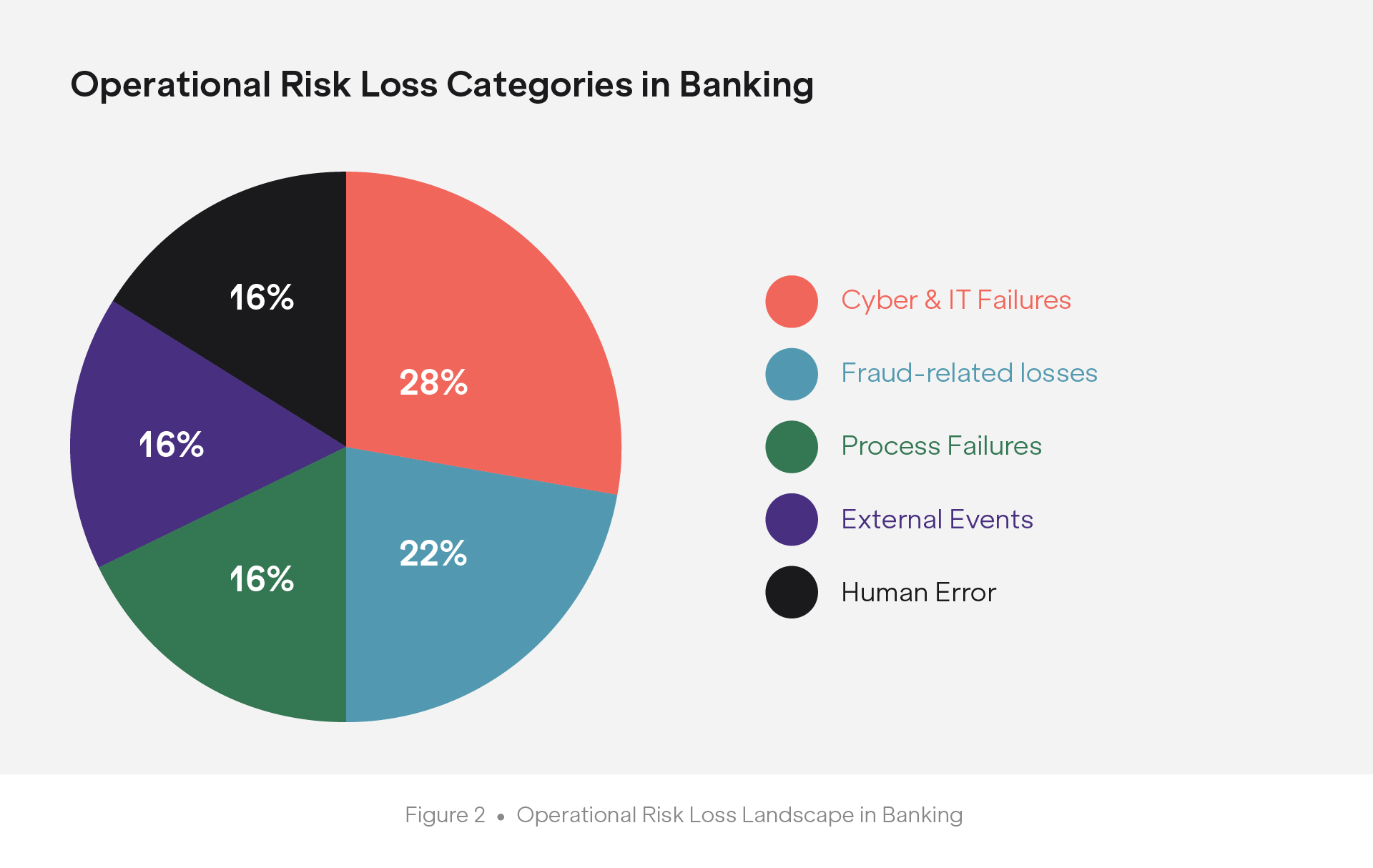

Operational Risk Management: Detecting Hidden Vulnerabilities

Operational risk encompasses process failures, human errors, system breakdowns, and external events. Cyber and IT failures now represent 28% of total operational risk losses, overtaking fraud as the largest category since 2023 [1]. Traditional operational risk management relies on manual reporting and reactive response, struggling to identify early indicators of control failures.

AI-powered monitoring implements continuous surveillance: tracking audit compliance, flagging insurance expiration and collateral drops; monitoring process execution, identifying backlogs and bottlenecks; assessing health control through staff turnover and system downtime. By establishing baselines and detecting real-time deviations, AI platforms provide early warnings of brewing crises.

The Basel Committee's Principles for Operational Resilience emphasize identifying interconnections that could disrupt operations—a requirement AI-driven monitoring fulfills more effectively than manual oversight [3]. Furthermore, 86% of financial services AI adopters indicate AI will be critically important to business success [4].

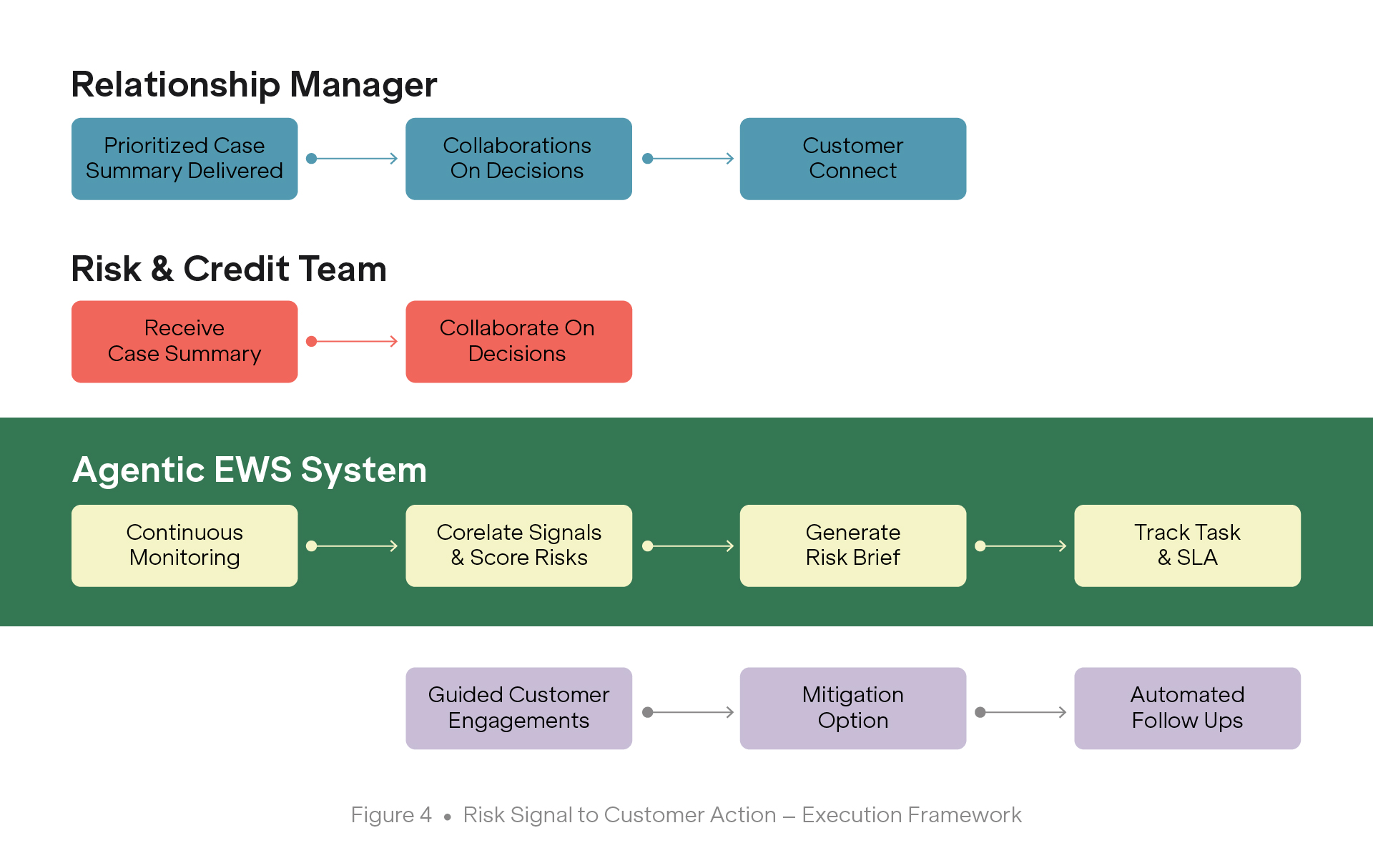

How AI Changes the Game: Agentic Architecture and Signal Intelligence

AI's transformative power stems from fundamentally different architectural approaches enabling intelligent collaboration and intelligent risk management systems. Agentic AI represents a breakthrough where multiple autonomous agents work in concert, each focusing on distinct risk domains, contrasting with monolithic rule engines. Specialized agents operate across the risk landscape: external risk agents monitor market data; internal risk agents track covenant breaches; financial risk agents evaluate liquidity and balance sheet deterioration across 24+ indicators; payment risk agents analyze transaction patterns; operational risk agents assess compliance gaps; and voice analysis agents extract sentiment signals.

With AI-powered credit risk management, each agent contributes findings to a recommendation engine that consolidates signals and generates mitigation strategies. This delivers critical advantages: higher signal-to-noise ratios by filtering irrelevant alerts; contextual correlation, combining weak signals into coherent cases [1]; and guided actions, recommending specific next steps. Effectiveness is reflected in adoption: 82% of mid-size companies and 95% of private equity firms plan to implement agentic AI by 2026, with 99% of early adopters reporting efficiency improvements [5].

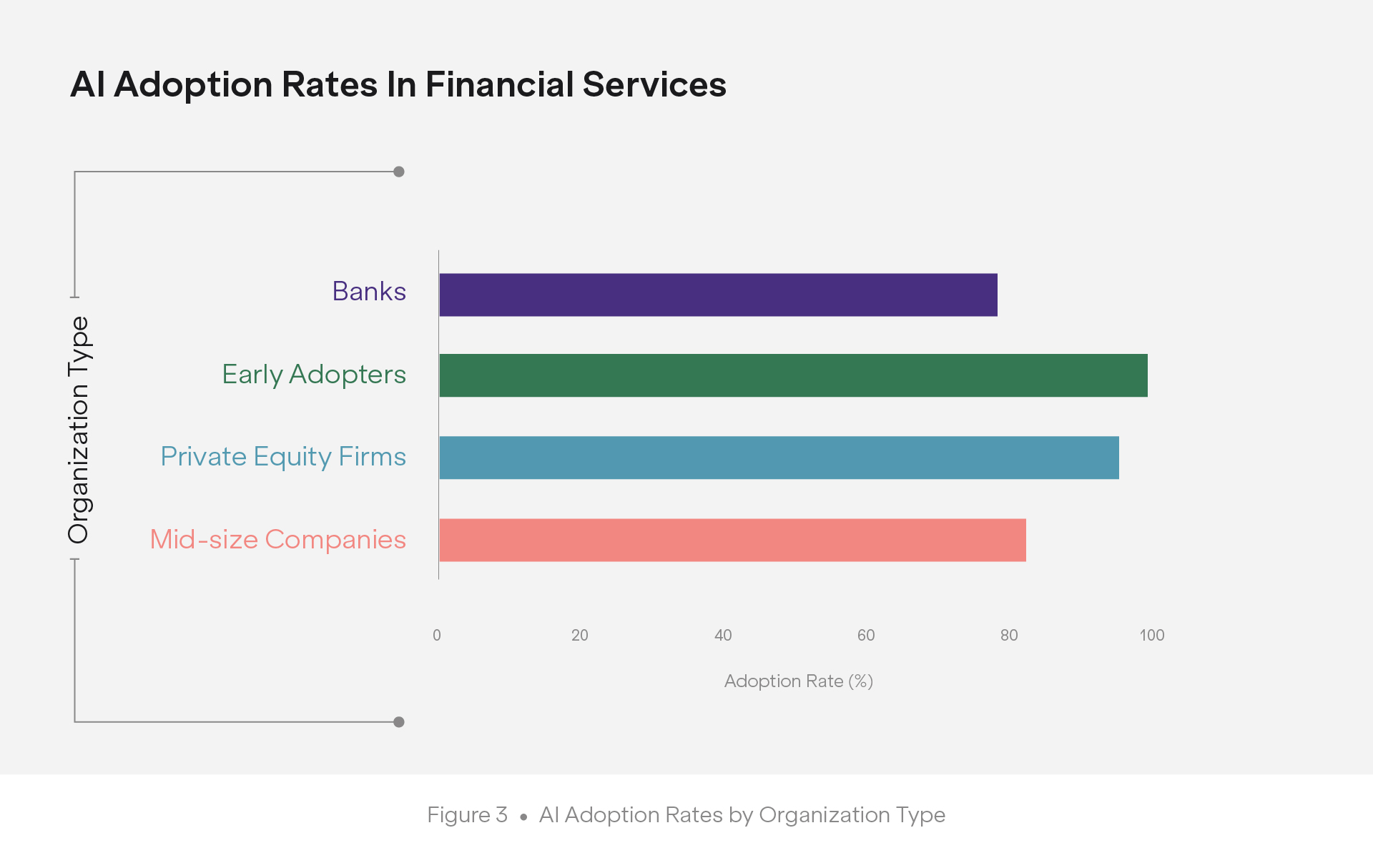

AI Adoption in Financial Services

The following chart illustrates AI adoption rates across different types of financial services organizations, demonstrating the widespread embrace of agentic AI technologies.

These high adoption rates across organization types—from mid-size companies to private equity firms and traditional banks—demonstrate the transformative impact of agentic AI on risk management practices. The near-universal efficiency improvements reported by early adopters validate the technology's ability to enhance signal detection, reduce false positives, and provide actionable risk intelligence.

Real-World Applications: From Theory to Measurable Impact

AI-powered early warning systems' practical value becomes clear through real-world implementations.

JPMorgan Chase's AI program has generated nearly USD 1.5 billion in cumulative savings [5]. The bank's COiN platform processes 12,000 commercial credit agreements in seconds—work that previously required 360,000 manual hours annually. CovenAce enables banks to analyze covenants 80-85% faster with up to 70% cost reduction [7]. These gains free teams for strategic work. Beyond efficiency, AI systems expand credit access while maintaining discipline. Capital One utilized AI to automate credit risk assessment, analyzing unstructured data to predict creditworthiness more accurately, achieving reduced losses and enhanced performance. Ant Financial developed AI-driven credit scoring analyzing transactional data and online behavior to assess creditworthiness in real-time, enabling rapid microloan extension to millions while minimizing defaults [8]. These applications illustrate a crucial principle: AI-powered systems don't simply replicate existing processes faster; they enable fundamentally different risk management strategies previously impossible at scale [1].

Conclusion: Building Resilience Through Intelligent Risk Management

The evolution from reactive monitoring to proactive AI-powered early warning with intelligent risk management systems represents a fundamental reimagining of how institutions protect value. The evidence is compelling: 92% of global banks reported active AI deployment as of early 2025, with AI expected to contribute USD 1.2 trillion to global banking by 2030 [2]. For credit risk, benefits include improved accuracy and earlier intervention preventing defaults. For operational risk, advantages include continuous surveillance detecting control gaps before they cascade, aligning with Basel Committee principles [3].

However, successful implementation requires more than deploying algorithms. Organizations must address data quality challenges and establish governance frameworks defining use cases, validating outputs, and maintaining human oversight as regulatory scrutiny intensifies. They should foster cultural shifts where professionals view AI as augmenting judgment rather than replacing expertise. Institutions navigating these challenges will gain competitive advantages: identifying risks earlier, responding faster, and allocating capital more efficiently. Most importantly, they'll transform risk management from a cost center into a strategic capability enabling profitable growth. As banking grows complex, the question is not whether to adopt AI-powered early warning systems but how quickly to implement them.

References

[1] Operational Risk Management in Banking: Ultimate 2026 Guide, Macmillan Education India Pvt. Ltd./IIBF, January 30, 2026.

https://riskpublishing.com/operational-risk-management-in-banking-basel/

[2] AI in Banking Statistics 2026: Powerful Growth - CoinLaw, Steven Burnett, July 2025: https://coinlaw.io/ai-in-banking-statistics/

[3] Operational resilience in banks | McKinsey, Anke Raufuss, Dan Williams and Thomas Poppensieker with Amrutha Ram Mohan and Marie Wahlers, October 21, 2025.

//https_www.mckinsey.com/?url=https%3A%2F%2Fwww.mckinsey.com%2Fcapabilities%2Frisk-and-resilience%2Four-insights%2Foperational-resilience-has-become-critical-how-are-banks-responding

[4] AI in Banking | Deloitte US, April 12, 2026.

https://www.deloitte.com/us/en/services/consulting/articles/ai-in-banking.html

[5] AI in Financial Services 2026: From Experimentation to Enterprise Scale, Blott, April 2026.

https://www.blott.com/reports/ai-use-cases-in-financial-services

[6] How AI will transform banking | McKinsey, December 09,2024.

[7] How AI is Reshaping Credit Risk Analytics and Compliance in U.S. Banks, Deloitte Insights, Oct 30, 2025.

PwC, Oct 16,2025.

https://www.pwc.com/us/en/industries/financial-services/library/how-ai-is-reshaping banking.html

CFA Institute, Feb 11, 2026.

https://rpc.cfainstitute.org/blogs/enterprising-investor/2026/ai-is-reshaping-bank-risk

[8] Case Studies of AI Implementation in Credit Risk | EOXS

https://eoxs.com/new_blog/case-studies-successful-credit-risk-management-practices/